Headline by Appointment

War and Peace

Way too many headlines this week to discuss and most ended up creating a lot of confusion regarding Iran and the potential for the Strait of Hormuz to re-open. My read is that the US/Iran peace negotiation process could easily get drawn out unless the United States seizes Kharg Island where Iran exports 90% of their oil. We will see if there are any updates over the weekend but the Strait looks to be closed as attacks and threats continue for any allies of the United States.

There are implications beyond oil which you can see below and I do have some commentary on the CFTC report from Thursday that shows how producers and speculators are positioned in the oil complex.

The S&P 500

If you have been following the chart below since last summer, the 7000 level was identified as technical resistance which now looks like a top. Prices moved steadily lower into the close on Friday as it seems the market is now beginning to price in a protracted Iran conflict. A lot of oversold readings so we could develop a bounce if there are positive headlines by Monday but momentum is beginning to accelerate to the downside.

Beyond Oil: What Else Gets Landlocked

The ongoing disruption at the Strait of Hormuz has dominated energy headlines, and for good reason—roughly one-fifth of the world’s seaborne oil supply passes through this 21-mile-wide chokepoint. But crude oil is only part of the story. The Strait is a critical artery for a surprisingly wide range of commodities that touch everything from your grocery bill to the semiconductors in your phone. Here’s a breakdown of what’s at stake beyond the barrel price.

The Bottom Line: A Hormuz closure isn’t just an oil shock—it’s a fertilizer shock, an LNG shock, a sugar shock, and an industrial materials shock all at once. The second-order effects on food prices, manufacturing supply chains, and technology inputs could be just as significant as the headline crude price move.

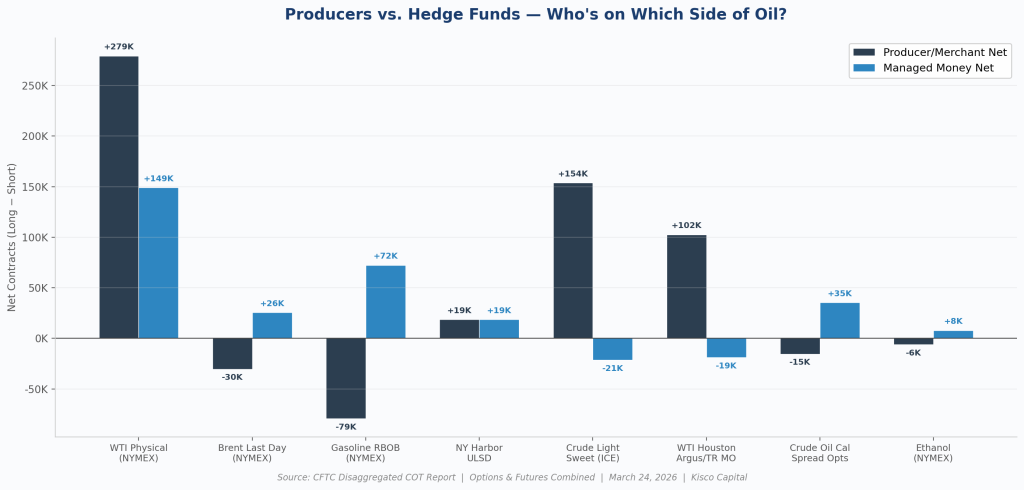

A Look At Oil Futures Positioning

The chart above breaks down net positioning across eight key petroleum contracts, comparing where oil producers stand versus where hedge funds are placing their bets. The most striking feature is WTI Physical, where both producers and hedge funds are net long — producers by +279K contracts and managed money by +149K. That’s notable because producers typically sell futures to hedge their output, so a large net long position suggests they may be repositioning or that the contract’s composition includes significant refiner activity on the buy side.

In RBOB Gasoline, we see the more traditional dynamic: producers are net short -79K contracts (locking in prices on their supply) while hedge funds are heavily net long +72K (betting gasoline prices head higher into spring driving season). Brent crude shows hedge funds net long +26K but producers slightly net short -30K, a more conventional hedger-vs-speculator setup.

The overall read: speculative money is leaning long on crude and refined products, but the positioning isn’t monolithic — there are pockets of bearishness in the spread and basis contracts that are worth keeping an eye on.

The Killing Joke: How will this all play out? What is the ending? Risk managers can identify oil spikes but commodity dislocations tend to fix themselves as price increases eventually result in demand destruction. In this situation, a military action caused the dislocation so it is much harder to see through the fog of war and the end to this blockade of the Persian Gulf. It does seem like the markets are approaching a fail-safe point to keep the contagion minimized. Experts say we have maybe 1-2 weeks until oil supplies get squeezed so time is running short. Tick-tock.

Thank you for being a reader!

President, Kisco Capital

This commentary is provided by Kisco Capital LLC for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Opinions are subject to change without notice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Kisco Capital and its clients may hold positions in securities discussed herein.