It's Getting Slippery

That happens with oil....

This was a week that began with cruise missiles over Tehran and ended with one of the worst jobs reports in recent memory. Oil is spiking, the Strait of Hormuz is effectively shut, and the labor market is cracking. There’s a lot to unpack. Let’s get into it.

Oil Surges Past $90 as the Strait of Hormuz Shuts Down

On February 28, the United States and Israel launched military strikes against Iran after a third round of nuclear talks in Geneva collapsed. The conflict is spilling across borders as Iran has bombed targets in Kuwait, Bahrain, the UAE, and Qatar.

The big issue is that ships are refusing to sail around the Strait of Hormuz for fear of attack from Iran. This has put oil exports at a standstill from the gulf states and Kuwait is shutting down production as they are running out of space to store oil. Other countries may soon have the same issue very soon unless they can move oil tankers safely from the area.

The issue is insurance and I did some research this week and created the graphic below to illustrate the complexity. The tankers have unlimited liability if their crew is harmed/killed OR if there is a spill that causes environmental damage. None will sail without the P&I insurance.

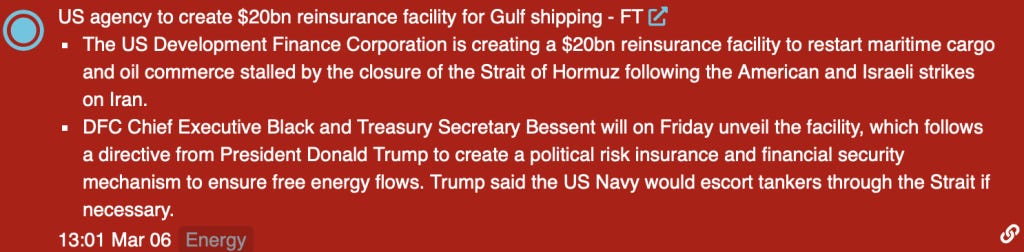

We did get the headline below on Friday afternoon so let’s see if it will work. The devil is in the details but this may get deliveries out of the gulf soon. $20B for re-insurance should be more than enough as the biggest of oil tankers costs $125-$150mm to replace but they take two years to build.

Inflation Expectations Will Rise

The big concern is an oil supply shock as WTI futures for April delivery spiked to $92.61 this week, up more than 30% from the lows near $56 hit in late February. A crazy spike as you can see in the chart below.

RSI is approaching overbought territory and the MACD has gone parabolic, but when tanker traffic through the world’s most important oil chokepoint grinds to a halt, technical indicators take a back seat to geopolitical reality. On the flip side, a reversal could be just as sharp.

For consumers, this translates directly to higher gasoline prices — the last thing a weakening labor market needs.

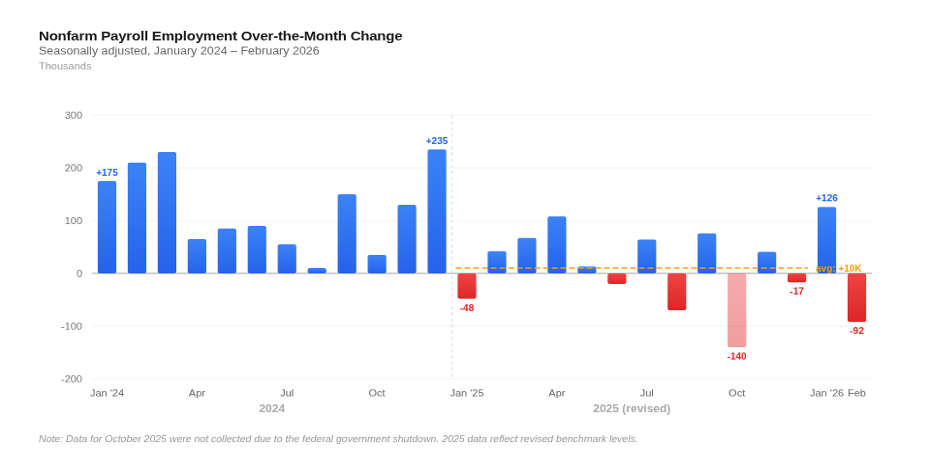

February Nonfarm Payrolls Slide

The February employment report showed we lost 92,000 jobs, a massive miss against consensus expectations of roughly +59,000. The unemployment rate ticked up to 4.4% and the labor force participation rate fell to 62.0%, its lowest level in over a year. The number of employed Americans dropped by 185,000 on the household survey while the ranks of the unemployed swelled by 203,000.

Beneath the headline, healthcare lost 28,000 jobs due to strike activity, federal government employment fell another 10,000 (continuing a decline of over 330,000 from the October 2024 peak), and manufacturing shed 12,000. The revisions were arguably worse: December was revised from +48,000 to -17,000, meaning the economy was losing jobs at year-end without anyone realizing it. January was trimmed from +130,000 to +126,000. Long-term unemployment continues to build, with 1.9 million Americans now out of work for 27 weeks or more — up 30% year-over-year.

The S&P 500 Is Holding Up

Despite all the challenges this week, the S&P held up relatively well. Slightly lower as you can see below in the upper right-hand corner. The momentum indicators show we are working off an overbought condition that peaked last October. So far, the price damage has been minimal but without relief from oil prices it wouldn’t be a shock to see a corrective pullback to the 6000 area.

Putting It Together

The jobs report tells us the economy was already weakening before the first bomb fell. Oil at $92 is a tax on every household and business in America. The Fed is caught between a labor market that needs easier policy and an energy shock that could reignite inflation.

Thank you for being a subscriber!

President, Kisco Capital

This commentary is provided by Kisco Capital LLC for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Opinions are subject to change without notice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Kisco Capital and its clients may hold positions in securities discussed.